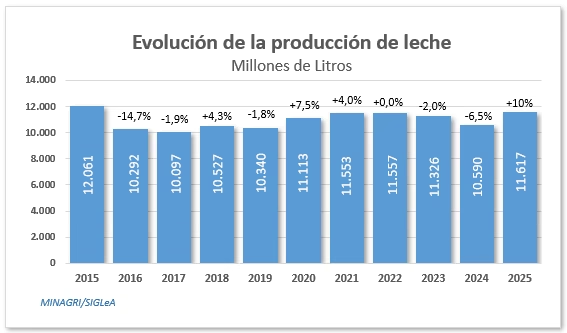

Milk production in Argentina recovered in 2025 the ground lost in 2024, confirming that the system responds quickly when climate, margins, and market signals align. According to SIGLeA/MINAGRI, national volume increased from 10.59 billion liters in 2024 to 11.617 billion liters in 2025, a year-on-year jump of 9.7% that offsets the previous decline (-6.5%) and places the sector back at high levels for the cycle (above 0.6% growth in 2022 and 0.5% growth in 2023). We ended the year with 8,895 dairy farms and 1,484,045 cows.

This growth, however, must be interpreted accurately: a significant portion is due to the "base effect," because 2024 was a year of depressed productivity. The full picture is best seen in the monthly figures. During 2024, year-on-year figures showed a prolonged period of decline, with very deep lows in the fall (double-digit drops). In contrast, 2025 began with a series of very strong increases, with year-on-year peaks of around 15% to 16% towards the end of summer/fall, before slowing down in the second half of the year to more moderate values (in the single digits). In other words: the year began with a rebound and ended with normalization.

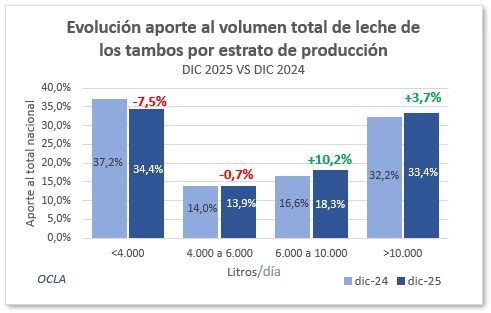

Now, the most relevant of 2025 is not only how much milk production grew, but who contributed. OCLA´s data by a liters/day stratum shows that growth was not homogeneous: smaller-scale dairy farms (<4,000 l/day) reduced their share of the national total from 37,2% to 34.4%while the strata of larger-scale expanded their weight, especially the segment of The 6,000–10,000 l/day (of By 16.6% 18.3%) and also the >10,000 l/day (of 32.2% to 33.4%).

This pattern suggests that by 2025 deepened the concentration processCosts are rising by 3% annually per liter of milk, and those who can't keep up face difficulties. Small dairy farms (<4,000 liters/day) saw a decrease of 7.5%, while the medium and large grew by +10.2% and +3.7% in In December 2025 compared to December 2024, the recovery was better captured, and feeding, management, and replacement strategies were sustained with greater financial resilience. Efficiency—liters per cow, diet stability, cost control, and management—remained the main determinant of the production landscape. On larger dairy farms (those with more than 10,000 liters per day average almost 20,000 liters per day), the cow is the last to notice market fluctuations.

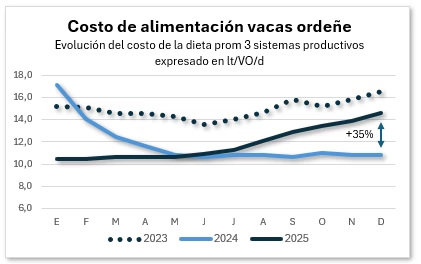

The following graph shows the sustained increase in the average feed cost for three production systems in Argentina. These costs, measured in liters of milk per cow per day, are approaching the levels seen at the end of 2023 that triggered the drop in production in 2024. Today, feeding costs are 4 liters per cow per day higher (+35% compared to last year):

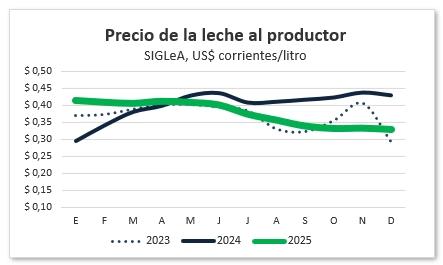

The producer has low prices similar to those of the end of 2023

Looking ahead to 2026, the most reasonable scenario is a moderate growth of 1% to 2%, conditioned by the evolution of the relative prices of milk/corn and milk/soy. With margins scarce or negative, the producer tends to prioritise liquidity and risk control before an aggressive expansion. That's why, 2026 is not projected as another year “bounce”, but, to mediate a correction in the relative prices, as a year of consolidation, where production will depend less on biological inertia and more on sustained profitability, the determining factor of which is the cost of feed.