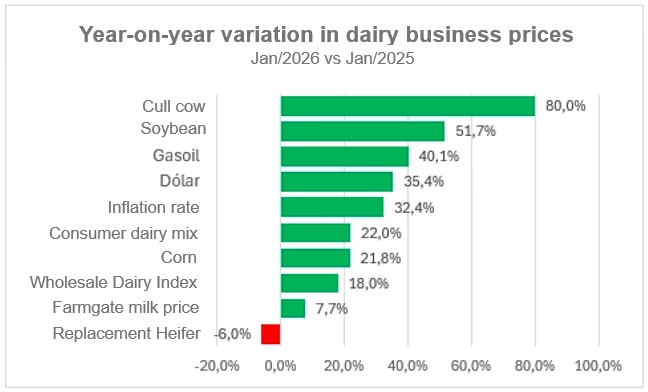

From June 2025 until the end of the year, the farmgate milk price in Argentina entered a plateau that surprised many dairy farms ($473/liter in June 2025 and $478/liter in January 2026). It wasn’t due to a single factor: supply, demand, and—above all—cash flow constraints all played a role. With historically high production, the system ran into a pre-election economy in crisis and a depressed domestic market. The result was simple: more product looking for an outlet in a weak consumption context. In this scenario, many dairy SMEs ended up overstocked. But the problem wasn’t only physical (full chambers and overflowing vats) but also financial: sustaining inventories with high interest rates pushes companies to liquidate. This led to cheese auctions and promotions to generate liquidity. At the same time, large industries stopped accepting milk from third-party producers, removing a buffer that usually stabilizes the primary market when there’s excess milk. The climate further hardened with business events that strained commercial credit: Verónica's pre-bankruptcy proceedings and signs of fragility in regional firms like La Suipachense, which heightened risk aversion along the chain. This led to January 2026 with the price of milk completely misaligned, arriving at a scenario similar to the end of 2023:

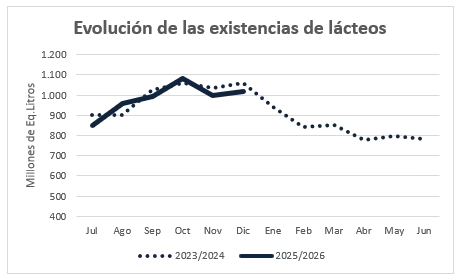

Over the months, the stock was gradually running out. By December, the market had normal dairy supplies for that month. This shift in balance supports the expectation of a price recovery in 2026: when the system stops “paying with stock,” the current supply becomes important again.

The producer's expectation is an essential readjustment of the milk price. It is interesting to review what happened in the mentioned 2023/2024 period. In the following graph, the dotted line corresponds to 2023/2024 and the solid line to 2025/2026. Important: stocks in both cases accumulated similar values in December (Dec/2023: 1,060 and Dec/2025: 1,015 million equivalent liters, -4%)

Looking at the evolution of the stocks, we think we are entering a new 'game' where we could tie the series (let's remember that the stocks summarize the information on Production – Export – Consumption + Import).

The production 2026 is falling sharply and will continue to drop until April-may, the economy stabilized and the sales better than 2024 with projection of growth, the micro is going to accommodate. The external market is bouncing back with a possible influence of chinese purchases and Brazil also starting to seasonal demand (by a difference of 20% between CIF Wholesale brazilian against the argentine FOB value) think about that sooner than later we will see an adjustment in the price of the raw material, which should round to 10-12% in the first half of the year