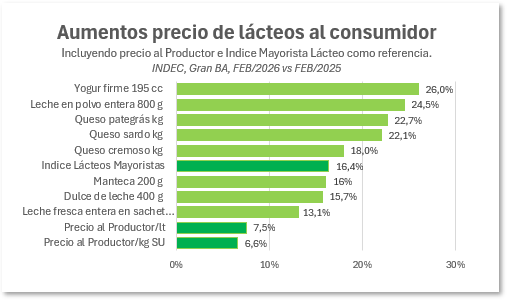

In recent months, a gap has solidified in the Argentine dairy supply chain that is difficult to ignore. While the industry maintains that the market is operating with a sufficient supply level for current consumption, price trends show that the pressure is not evenly distributed among the different links in the chain. Looking at the year-on-year comparison to February 2026, the most striking data point is the disparity between the price paid to producers and the price evolution of the rest of the supply chain. The price of milk at the farm gate rose by just 7.5% per liter and 6.6% per kilo of useful solids (fat + protein), well below the Wholesale Dairy Index, which advanced 16.4%, and even further from several consumer products: firm yogurt 26%, whole milk powder 24.5%, pategrás cheese 22.7%, sardo cheese 22.1%, cream cheese 18%, butter 16%, dulce de leche 15.7% and fresh milk in sachets 13.1%.

821 If these variations are further weighted according to the milk's processing destinations in Argentina, the picture becomes even more telling. Approximately 50% of the milk is used for cheese, 29% for powdered milk, 15% for fluid milk, 3% for yogurt, and 3% for other products. Under this weighting, the dairy mix for consumers shows a year-on-year increase of around 22%. In other words, the value of dairy products has risen at a much faster rate than that of raw materials. Of course, this comparison doesn't allow for a simplistic conclusion. Between the dairy farm and the supermarket shelf, there are costs associated with processing, packaging, logistics, taxes, marketing, and financing. But even considering these factors, the gap is too wide to ignore the unequal distribution of value within the supply chain.

It is important to note that the period analyzed coincides with a phase of lower relative supply, which makes it less convincing to attribute the price lag to the producer solely to an alleged abundance of milk.

A new tension is also emerging for many Argentine companies. With a more stable macroeconomy, managing timelines, inventory, and working capital is no longer enough. Success increasingly depends on producing, processing, and selling more effectively. The problem arises when this transition isn't resolved solely through internal improvements, but also by keeping raw material prices significantly lower. If the problem were solely an inability to absorb or sell the milk received, one would expect more visible signs of reduced milk intake. However, raw materials continue to be received, processed, and sold, while the price paid to producers remains far behind the industrial value and the final retail price.

In short, the chain showed ability to recompose prices, pero esa mejora no llegó con similar intensidad al tambo. Y cuando eso se prolonga en el tiempo, las consecuencias son conocidas: menor rentabilidad, descapitalización, inversiones postergadas y menos incentivos para sostener el crecimiento productivo.

Es muy claro tu mje Marcos. Se me ocurre q aparte seria conveniente tener algun instrumento para busqueda de financiación con bancos h otros agentes , por ejemplo q la liquidacion sea quincenal o cada diez para ofrecer como gtia, especie se fact de crédito. Es una idea, debe haber más.

exportar más leche en polvo,

mozzarella,

otros productos,

y, pensar en una estrategia exportadora pais, ej. Nueva Zelandia

Adelante Marcos, poniendo a la luz la situación de la cadena, es un paso importante, ya va a dar sus frutos