The interest of this note is to compare the dairy argentina with the case uruguayan neighboring country producer and exporter of milk, to see what the issues are common to both dairies and which are purely domestic issues.

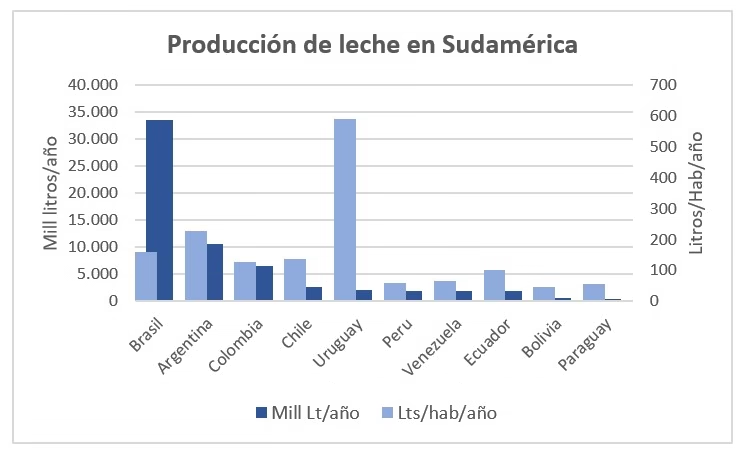

To put in context, recall that Argentina, see graphic Production of milk in South america, is the second largest producer of milk behind Brazil, has the drums more big, is the largest exporter in the region, and 3° exporter of milk powder on the planet. Uruguay is the 5th largest producer (behind Brazil, Argentina, Colombia and Chile), but the 2nd exporter of dairy competing with Argentina in the international trade of milk powder (LPE). This is not for less, since Uruguay is the country with 590 lt/Hab/year, producing more milk per capita in South america. They also have milk consumption highest in the region, 266 lt/Hab/year, but their abundance and need to be exported 77% of what they produce.

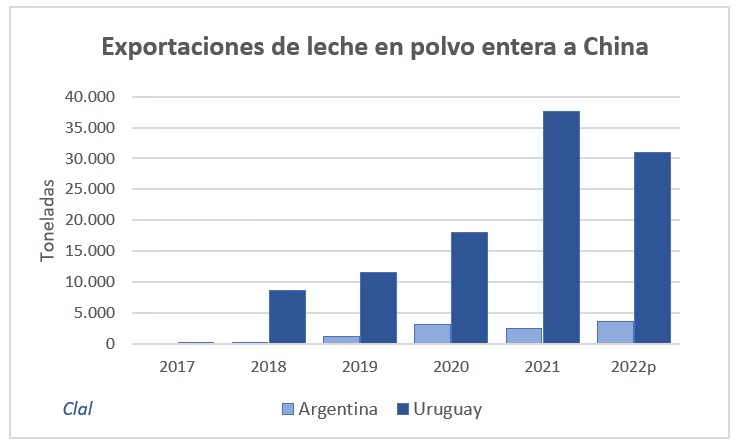

Uruguay, with 5.6 million litres of milk/day, it produces about 70% of that produced in the province of Buenos Aires, our heels in the export of LPE. In 2021 we exported to Brazil 28.865 tons of LPE (+17% of the volume exported by Argentina to the country), and in 2022 (jan-oct) collects 22.216 ton a -35% less than the shipments from Argentina to Brazil. But it's very interesting to see what is exported by both countries to China, while Argentina leads sold to the Asian Giant between jan-sep. 2022 few 3.542 tons of LPE, Uruguay builds up a sale, in the same period, of 23.280 ton moving to Australia as a second supplier of China from 2021. Have been working in competitiveness for years, and even, lately, dealt with a possible free-trade agreement with the asian.

When you mention the “competitiveness” is often thought of in the performance of the tandem-primary production and processing industry. But when it comes to export competitiveness does not only involve the producer and the industry, but also the State with its controls, its taxes, and the public policies necessary to facilitate the task and ensure the inflow of foreign currency.

Being at the same distance of China, both countries it is inferred that the difficulty of argentina to increase its volume exported is due to the lack of export competitiveness caused by a State unhelpful. The dairy chain to argentina has a link of primary production in a highly competent all time that works and grows with the prices of raw material lowest in the world, and the link local industrial capacity to efficiently process the volumes necessary to compete with and to supply the internal and external market. But it is a drag to include the heavy-argentine State with your pressure outright tax as are the Rights of Export among others (9 % for the SBA, the main dairy exported), and the indirect as the backlog of foreign exchange (minimally 30% and the unusual range of types of dollars fictitious existing) in addition to the inflationary tax (the COVID and the war affects everyone, but Uruguay has an annual inflation rate of 9% while Argentina 83%).

Without a doubt it would be hopeful that the current Administration and those yet to come will replantearan seriously change the way you do things in order to generate the long-awaited revival is not only dairy argentina (represented by 10.446 drums, 670 processing companies and 187.000 employees guessing), but of the economy as a whole.

NdR: Note published in the magazine Chakra

[twitter-follow screen_name=’dairylando’]