At the gates of the spring 2021, what we call "prior", and as in each spring of memory, there arise the questions about the development of the business, production, exports, consumption and...the price of milk to the producer. Added to all this, each of the both is added to the seasoning political, as would be the case of the general elections on 14 November. The policy intervention is currently affecting the dairy sector strongly in three areas, as are the rights of export (currently at 9% for the milk powder and 5% for the cheeses), the closure of export of meat that stuck to strong sales of cows refugo in the drums (the famous "cow of china") and the backwardness of the type of change that is already posted around -16% lower than that was the official dollar in August 2020 (constant currency).

In the preview of this year (July-August 2021) come with the economy revived, comparing with the one we had in 2020 at this point, with the expectation of a 2nd half with greater liquidity in the pockets of the consumer, and, if the last year with full pandemic consumption grew by +2%, well there could be something similar in this period. A GDP growth of +7% would indicate a growth in consumption of dairy of +3.5% in 2021 over 2020. Besides consumption, we have a variety of interacting factors on the supply and demand of milk with which we put together the following chart comparing the evolution of each factor with its level to "prior" 2020:

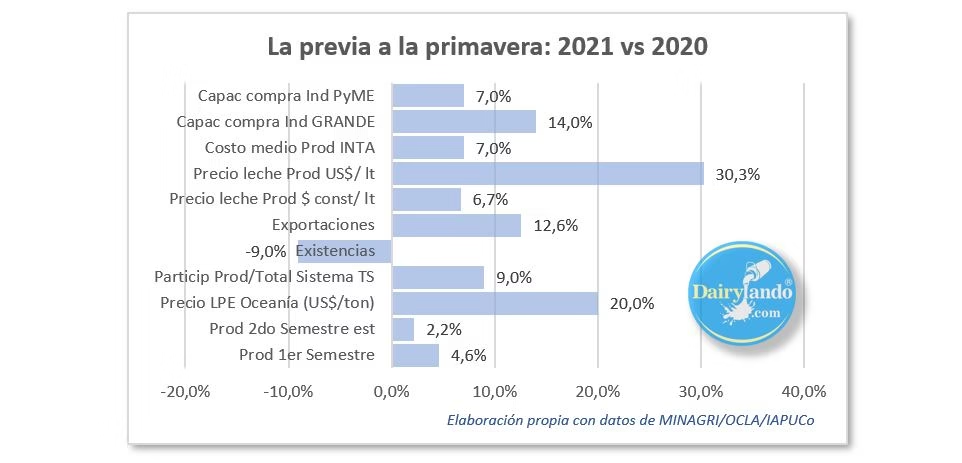

From the side of the primary production, the tambero, we observed an improvement in real terms of the price of the milk +6,7% (jul/aug), while their cost grew up in the same currency +7% (jun/jun), a large part referenced to the cost of feeding with milk price as of July tambero costs +14% the purchase of corn for their cows that what it cost in July 2020. Now in terms of US$/lt and due to the delay of the official exchange rate, that increase of +6.7% in constant pesos goes to +30% measured in dollars per liter. The producer price in dollars is located in the top decile of the records in that currency. It is also to be noted that with 36.6 per cent for June, the participation of the producer this above the 31% average of the records of IAPUCo 2013-2021.

By the side of the industrial sector, we observe an improvement in their purchasing power with respect to the last year (according to IAPUCo in June 2021: +7% for Smes and +14% for the Large). Despite the increasing prices in dollars for the raw material, we have been exporting +12.6% in equivalent litres of the same period (jan-jul) last year ( -OCLA), helping to do this the best price of milk powder that records +20% on values of the previous (August 2021 vs 2020). For our peak month, October, the future of NZX suggest a value of +17% higher than in October 2020. Obviously it would be very good for a reduction in withholdings as well as are remaining in the string 4 $/l, a value that would be used to the price to the producer or to recover a little the loss of -6% for the industrial participation in the values of the consumer (IAPUCo, Total System). Here comes the peak of milk production which the target should be to the outside. We estimate a production for the 2nd semester 2021 +2.2% in about 2020 if the curve keeps the current trend (closing the year with a total volume +3,3% higher than the one for 2020). It is an incentive that the stock would a volume -9% lower than the prior year 2020. With all of the above, we might expect to be able to export that milk as it did last year...more concerned about the logistical issues raised by the shortage of containers.

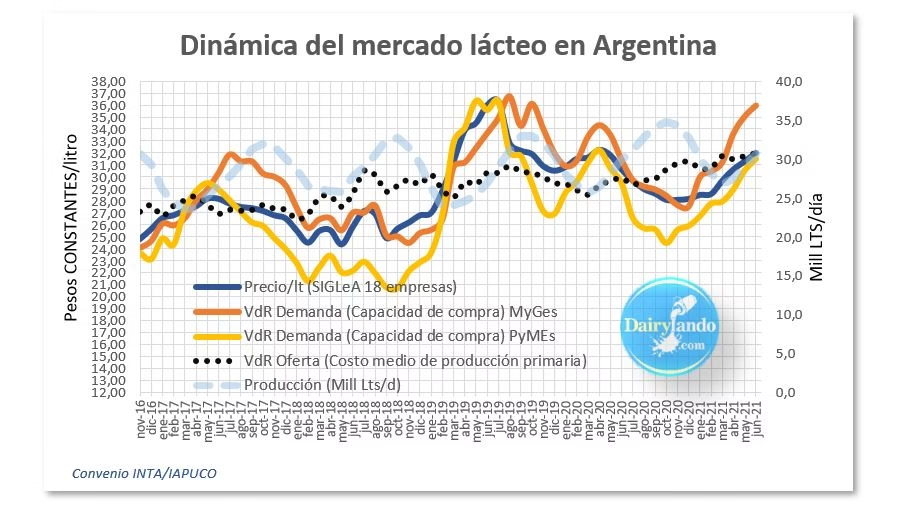

We will wait to see as it continues to evolve the dynamics of the dairy market argentino until June 2021 are presented as follows:

During the first half of 2021 the price increases perceived by the production came in above the rate of inflation. Starting in July, we saw an adjustment of price that does not cover the inflation. It is expected that the following adjustments to maintain the purchasing power until the dollar is starting to recover...maybe November...we'll see.