We are in transition to a very grave crisis, a crisis equal to or worse than the 2001.

70% of the costs of milk production are tied to the dollar and we are on the verge of a sharp devaluation.

Immersed once again in a perfect storm of the dairy chain all cracks in front of the striking effects of the inability of the public administration of the last 100 years. The description of this inability makes it very well Tato Bores in his monologue about the devaluation, so we left it there and we will have to the situation of the dairy argentina.

Ya con la devaluación post PASO el costo de los granos se disparó a niveles poco vistos desconfigurando los precios relativos con la leche. En el siguiente gráfico, “Frecuencia de la relación maíz y leche”, observamos que mientras el 80% de la serie 2001-2023 el poder de compra del maíz se mantuvo entre 1,50 y 2,50 kg/lt de leche promediando históricamente 2 kg de maíz/lt, en la actualidad (punto rojo) la relación se ubica en un valor poco observado (<10%) se 1,25 kg de maíz/lt de leche.

The corn is indispensable in the production of dairy and represents generically the account of expenses in the power of the rodeo dairy, note that it takes 60% of the direct costs dairy farmers.

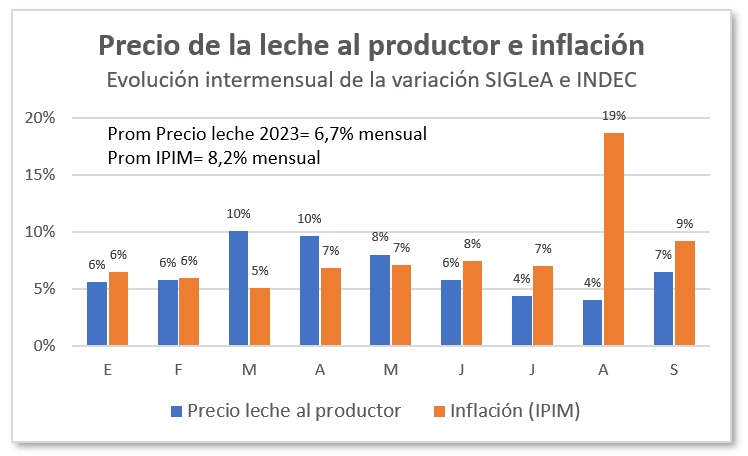

The price of grain will hardly go down as shall be tied to the variation of the type of change that is, at the time of writing this note, to the point of the jump (because of the delay to which they have attached). Today, to carry the milk to a purchasing capacity of 1.5 kg of corn needed a producer price 145 $/lt and to reach the historical average of 2 kg of corn/lt of milk, the price should be of 194 $/lt. This requires increases of between +21% and +62%, respectively, when from June producer prices were adjusted for under inflation.

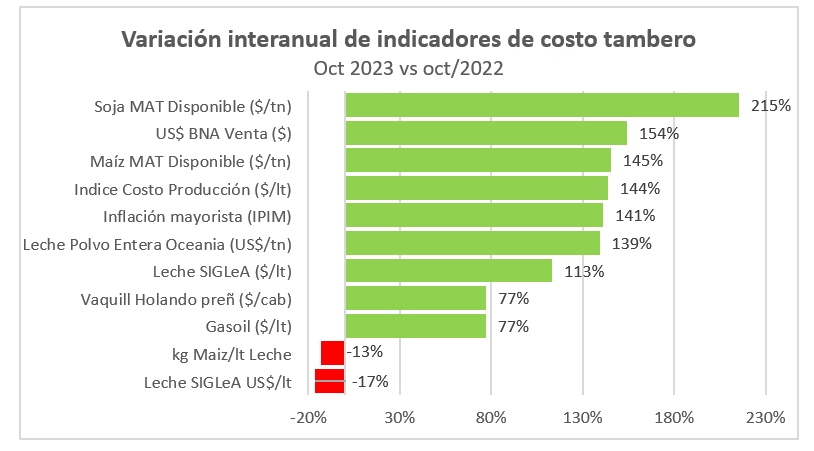

In a pan with indicators selected drivers of the cost tambero we look at the backwardness of the price of the raw material, largely attributable to the settlement price of the industrial sector in the State that will expire as soon as possible:

In a year with something less milk, we estimate for the first half of 2023 a missing 320,000 lt/d compared to last year, a trend that will be exacerbated in the 2nd half. Among the causes of the deterioration of the price of milk to the producer we observe a reduction of exports to Brazil which has led to an accumulation of stocks that balance the shortage of milk. The impact is noticeable due to Brazil traveled to Algeria as the main destination for exports of milk during the year 2023 absorbing the 46% of the total tonnage exported:

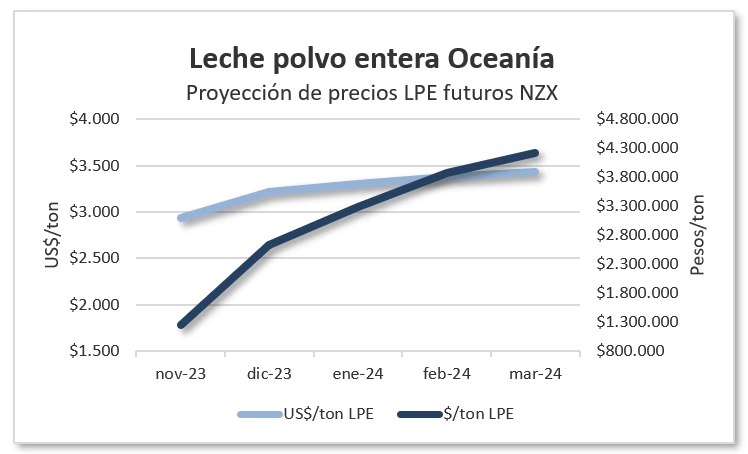

As of October, the scenery begins to change, were eliminated Export duties which were remaining 9% of the sales of milk powder and 4.5% to the cheese and is adjusted to the official dollar a +20%. To this is added the recovery of the international marketplace with a growing trend of operations in the future. Seeing this, and combined with the future Rofex for the official us-dollar begins to shine a light of hope at the end of the tunnel, a potential business exporter that traction to the price of milk to the producer. In the following chart, we measure the impact on the ability of the purchase of raw materials destined to the elaboration of milk powder, with 61% of the total volume of liters are exported, it is the main dairy products exported by Argentina. Note the level lean that presents November, the month in which only a sharp drop in production could generate some pressure to the milk, but as of December, enters a new dimension whose impact will be limited only by the drying capacity of around 30% of the national milk.

[twitter-follow screen_name=’dairylando’]