Argentina meets exceptional conditions to consider it a power milk. Its vast plains with soils are deep and fertile, combined with a temperate climate and abundant availability of water, allow to produce high-quality forages at very low cost. On this basis, the producers are free to choose the production system that best fits the availability of resources and their productive vocation: from grazing style of New Zealand, highly efficient in the use of the land, until the intensive confinment systems comparable to the best in the United States, with high levels of technology, automation and comfort animal. The dairy industry in Argentina has made strong investments in processing plants, logistics, and technology, and maintains expansion projects to increase the capacity of processing and remain among the major dairy exporters in the world. This positions the country not only as a reliable supplier for their domestic market, but as a future exporter relevant powdered milk, cheese and other value-added products to the world.

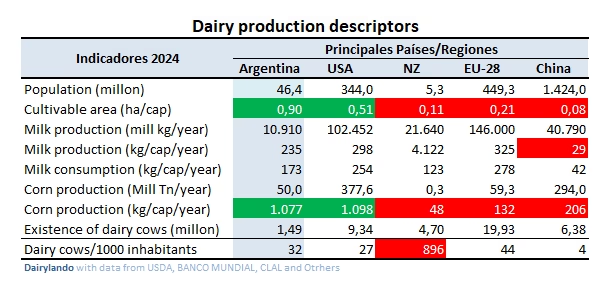

To put in context it is interesting to note the following table where we analyze indicators of competitiveness between countries and regions involved in the production of milk and to include China as a major importer of dairy products on the planet:

Argentina's vast arable land is a key feature, boasting nearly one hectare per capita (with the corn belt in United States and a strip in central Europe is one of the three most fertile plains in the world). The country carries a capacity to produce abundant corn (grain or silage) and alfalfa that are the main ingredients in the diets of high production cows. The climate, rainfall and soils allow the double annual crop. Thanks to the low density of cows, environmental problems like those seen in Europe and New Zealand are not observed in Argentina.

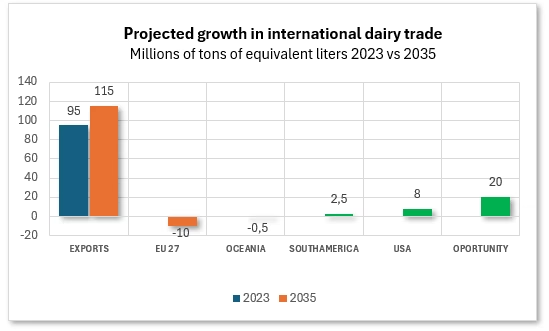

In the following graph, with Rabobank data, we see that it is expected that within 10 years we´ll find ourselves with an unmet demand of 20,000 million litres of milk (almost double of Argentina´s actual production):

This graph is referred to the international trade of dairy products, expressed in litres/tonnes equivalent milk. Assumes:

- Global demand to grow about 20 Mt LME additional to 2035.

- Minor contribution exporter EU-27 and Oceania (-10 and-0.5 Mt).

- Greater participation of EE. UU. (+8 Mt) and South america (+2.5 Mt).

- A space of ~20 Mt of “opportunity” cover for new sources, or for greater efficiency in the current. The eyes are on Argentina and the united States.

The OECD-FAO Agricultural Outlook 2025-2034 projected that the global trade of dairy products (in weight product) will grow around 12 % until 2034, continuity of the triad of export to EU–EE. UU.–NZ, and with the united States as the exporter large more dynamic, while NZ and the EU are more limited by environmental issues and costs. FAO/IDF and other works agree that the global consumption of dairy maintains a trend of growth close to ~2 % annual in the long term, traccionado in Asia and Africa, even with something less push in China.

The global demand for dairy products is increasing; we prepare to provide it with efficiency, quality, caring for the environment and human and animal welfare.